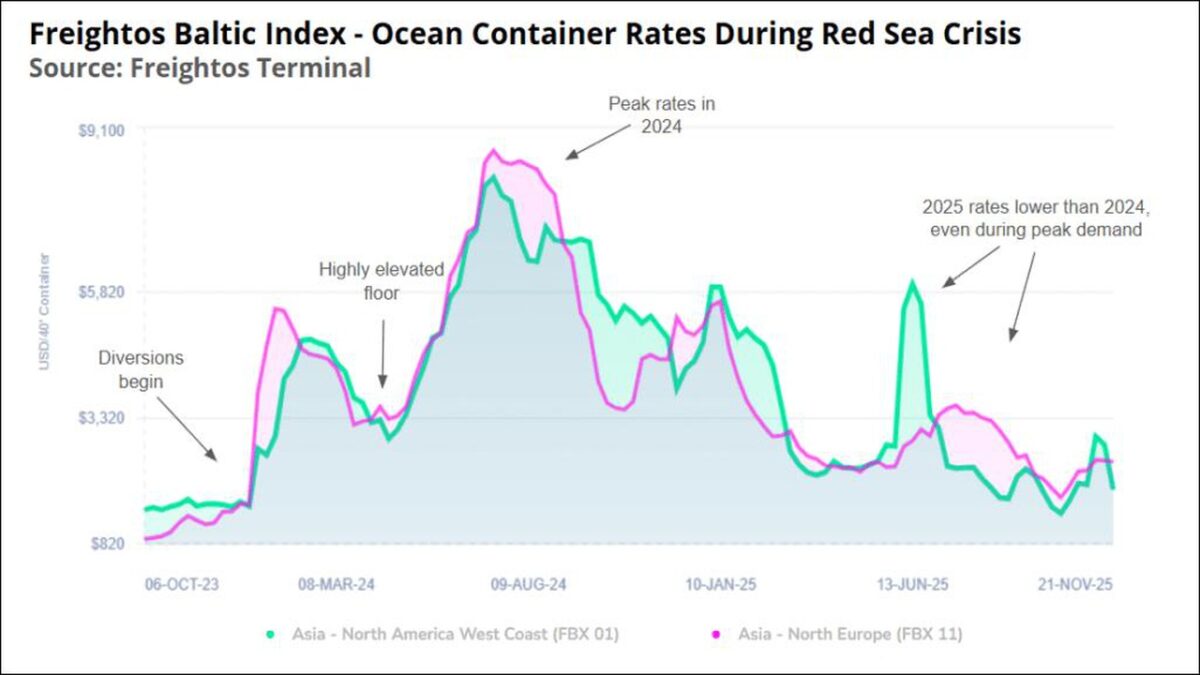

Global Container Freight Index Continues Downward Trend | Mariner News

The global shipping landscape is experiencing a significant shift, with the container freight index continuing its pronounced downward trajectory. After reaching unprecedented highs during the peak of the pandemic, these crucial benchmarks for maritime shipping costs have been in a consistent state of decline, signaling a return to more normalized market conditions, albeit with potential challenges for carriers. This sustained weakening of the index reflects a complex interplay of evolving supply and demand dynamics, economic headwinds, and the gradual untangling of congested global supply chains that characterized the past few years. For businesses and consumers alike, understanding the implications of these falling freight rates is paramount, as they directly influence the cost of goods and the profitability of global trade routes.

This ongoing descent of the container freight index is more than just a statistical blip; it represents a fundamental recalibration within the world of container shipping. The exponential rate increases observed between late 2020 and early 2022, fueled by surging consumer demand for goods, port bottlenecks, and limited vessel capacity, created an environment of extraordinary profitability for ocean carriers. However, that era appears to be firmly in the rearview mirror. Today, major composite indices, such as the Shanghai Containerized Freight Index (SCFI) and the Drewry World Container Index (WCI), regularly report week-on-week reductions, often bringing spot rates below long-term contract rates and, in some cases, even below pre-pandemic levels. This sustained decline paints a clear picture of a market grappling with overcapacity and diminished demand.

Unpacking the Decline in Container Freight Index

To fully grasp the current market sentiment, it’s essential to understand what the container freight index represents. These indices track the average spot market freight rates for shipping containers on key global trade routes, typically expressed per forty-foot equivalent unit (FEU). They serve as vital barometers for the health and cost efficiency of global logistics and maritime trade. Their recent nosedive stands in stark contrast to the historical peaks witnessed, when rates on lucrative routes like Asia-Europe or Trans-Pacific soared by over 1,000% from their traditional baselines. This historical context underscores the magnitude of the current market correction.

The decline isn’t merely a minor adjustment; it’s a significant unwinding of the pandemic-era surge. For instance, rates on key routes have plummeted by 80-90% from their peaks, marking one of the sharpest corrections in recent shipping history. This substantial drop is primarily driven by a fundamental shift in the supply-demand equilibrium. During the pandemic, an insatiable demand for physical goods, coupled with severe operational inefficiencies at ports and inland logistics hubs, created an artificial scarcity of shipping capacity. Now, with those factors largely reversing, the market is aggressively correcting itself.

Key Factors Driving Lower Container Shipping Costs

Several interconnected factors are contributing to the downward pressure on container shipping costs and the resultant fall in the container freight index. One of the most significant is the softening of global consumer demand. Post-pandemic, there’s been a noticeable pivot from goods consumption back towards services, exacerbated by persistent high inflation and rising interest rates globally. This economic environment has dampened consumer purchasing power and confidence, leading to reduced orders from retailers and manufacturers, which directly translates to fewer containers needing to be shipped.

Another crucial element is the significant alleviation of supply chain disruptions. The notorious port congestion that plagued major global gateways like Los Angeles, Long Beach, and Rotterdam has largely dissipated. Vessels are now spending less time waiting to berth, and container turnaround times have improved considerably. This enhanced operational efficiency effectively increases the available vessel capacity in the market, as ships are no longer tied up in queues, allowing them to complete more voyages. The smoother flow of goods through ports reduces demurrage and detention charges, further contributing to lower overall freight rates.

Furthermore, the influx of new vessel capacity is a critical supply-side factor. During the boom years, carriers placed massive orders for new container ships. Many of these mega-vessels are now being delivered, adding substantial tonnage to the global fleet. This increased capacity, entering a market with subdued demand, inevitably creates an imbalance, forcing carriers to compete more aggressively on price to fill their ships. While some carriers are implementing blank sailings (cancelling voyages) to manage capacity, the sheer volume of new vessels makes it challenging to maintain freight rate stability without substantial demand recovery.

Finally, broader economic headwinds and geopolitical uncertainties play a role. The specter of a global recession, ongoing conflicts, and persistent inflation concerns create an environment of cautious spending by businesses and consumers. Many retailers, having overstocked during the pandemic, are now working through existing inventories, reducing the immediate need for new shipments. This inventory overhang has significantly contributed to the reduced demand for maritime shipping, pushing liner indices lower.

Navigating the Ripple Effects on Global Logistics

The continued decline in the container freight index has far-reaching consequences across the entire global logistics ecosystem. For shippers and beneficial cargo owners (BCOs), particularly retailers and manufacturers, this trend is largely a welcome development. Lower shipping costs directly translate into reduced expenses for importing goods, which can improve profit margins, allow for more competitive pricing strategies, and potentially alleviate some inflationary pressures for consumers. It also offers greater predictability in budgeting and planning, moving away from the volatile, premium-laden environment of the past.

Conversely, ocean carriers are facing significant pressure on their profitability. After enjoying record earnings, they are now grappling with rapidly declining freight rates, which are eroding their margins. This situation could lead to various strategic responses, including further blank sailings to manage capacity, slow steaming to save on fuel costs, and even scrapping older vessels. There might also be a renewed focus on securing long-term contracts at sustainable rates and exploring vertical integration opportunities to control more aspects of the supply chain. The competitive landscape will intensify, potentially leading to consolidation or changes in alliance structures as carriers strive to maintain viability in a tougher market.

Freight forwarders, who act as intermediaries between shippers and carriers, are also adapting to this new reality. While lower rates can reduce their sourcing costs, they also face pressure to offer competitive pricing to their clients. Their value proposition will increasingly hinge on their ability to provide integrated logistics solutions, superior customer service, and efficient supply chain management rather than simply securing capacity at any cost. This market shift also potentially benefits consumers, as lower import costs can eventually translate into more affordable prices for a wide array of goods, ranging from electronics and apparel to household items.

The Future Outlook for Container Freight Rates and Trade

The critical question now facing the industry is whether the current downward trend in the container freight index represents a return to pre-pandemic normality or a descent into a prolonged period of extremely low rates. Most analysts predict that while the extreme highs of the pandemic are unlikely to return anytime soon, the market will eventually find a new equilibrium. However, the path to that equilibrium may be bumpy, characterized by continued volatility and intense competition among ocean carriers. Factors such as global economic recovery, unforeseen geopolitical events, or new environmental regulations could influence the speed and direction of future freight rate movements.

There are several scenarios that could influence the future of container shipping. A stronger-than-expected rebound in global economic growth and consumer demand could stabilize or even slightly increase rates. Conversely, a deeper or prolonged global recession could push rates even lower, potentially leading to significant financial challenges for less resilient carriers. Furthermore, the industry is grappling with new environmental regulations, such as the IMO’s Carbon Intensity Indicator (CII), which could impact operating costs and vessel speeds, thereby affecting available capacity and potentially shipping costs.

In the long term, the global logistics landscape is likely to evolve towards greater resilience and technological integration. Shippers are increasingly diversifying their supply chain strategies, exploring near-shoring or friend-shoring options to mitigate risks. Carriers will continue to invest in digitalization and efficiency improvements to optimize operations and reduce costs. While the days of sky-high freight rates may be over, the industry remains dynamic, with new challenges and opportunities constantly emerging. Monitoring the container freight index will remain crucial for all stakeholders navigating this complex and ever-changing environment.

In conclusion, the sustained downward trajectory of the container freight index marks a significant turning point for the global container shipping industry. It signifies a market correction from unprecedented highs, driven by softening demand, resolved supply chain disruptions, and increasing vessel capacity. While challenging for carriers, this trend offers much-needed relief to shippers and promises a more stable, albeit highly competitive, future for maritime trade. All stakeholders must remain agile and informed to navigate the evolving dynamics of global freight rates and logistics costs effectively.