Singapore Bunker Sales Decline 7.4% in May Analysis | Mariner News

Singapore, the undisputed global bunkering hub, recorded a notable contraction in its marine fuel sales for May, experiencing a 7.4% year-on-year drop. This decline in Singapore bunker sales signals potential shifts in the dynamic global shipping fuel market, prompting close scrutiny from industry stakeholders and maritime commerce participants worldwide. While total sales did show a modest recovery from April figures, they remained significantly below the robust volumes observed in March, a period that saw an unexpected surge in demand driven by geopolitical events. This recent data, released by the Maritime and Port Authority of Singapore (MPA), offers a critical snapshot of the current health and evolving trends within the world’s largest ship fuelling station. Understanding the nuances behind this contraction is crucial for forecasting future demand.

Analyzing the May Decline in Singapore’s Marine Fuel Market

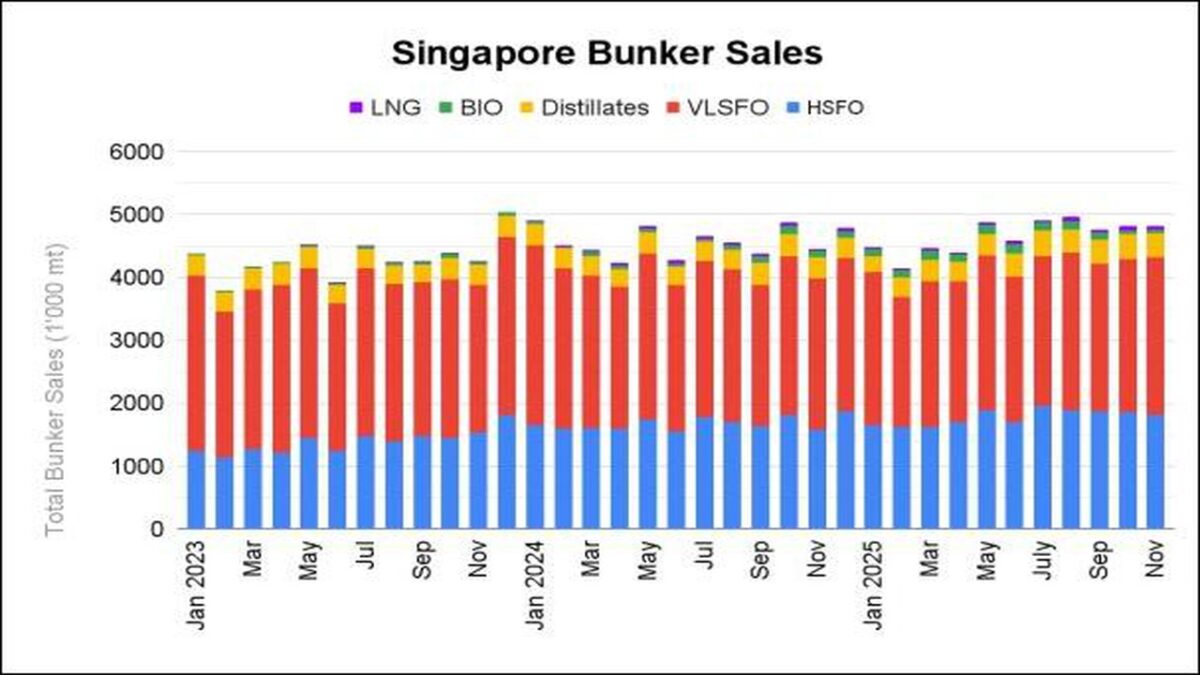

The latest statistics from the Maritime and Port Authority of Singapore (MPA) reveal that May’s total demand for conventional and biofuels in Singapore reached 4.48 million metric tonnes. This figure represents a 7.4% decrease compared to the same month last year, although it marked a 3.9% increase from April’s volume. However, the total still fell short of the 4.72 million metric tonnes registered in March. The earlier surge in March was notably influenced by the outbreak of the Iran war, which led to a temporary boost in bunker demand within Singapore as vessels rerouted or front-loaded their fuel purchases amidst heightened uncertainty. This comparative analysis underscores the volatility that external geopolitical factors can introduce into an otherwise stable market, significantly affecting marine fuel sales volumes.

Industry experts are closely examining whether this year-on-year drop indicates a sustained downward trend or merely a temporary fluctuation within the Singapore bunkering hub. Factors contributing to reduced demand could include shifts in global trade routes, slower economic growth impacting shipping volumes, or increased competition from other regional bunkering ports. The sustained pressure on operational costs for shipping companies means every percentage point shift in fuel consumption is significant. Therefore, the dip in Singapore bunker sales warrants a deeper look into its underlying causes. These trends are not isolated; they reflect the intricate web of global maritime commerce and the constant adaptation required in the shipping fuel market.

Diverse Fuel Performance: Conventional, Biofuels, and LNG Bunkering Trends

A more granular look at the May data reveals varied performance across different fuel types. Very Low Sulphur Fuel Oil (VLSFO) sales, a primary fuel choice for many vessels, saw a 6.5% decline compared to May last year. High Sulphur Fuel Oil (HSFO) sales, typically used by scrubber-equipped vessels, also experienced a downturn, dropping by 5.2% over the same period. These figures indicate a broad-based reduction in conventional marine fuel consumption, suggesting that the overall decrease in Singapore marine fuel sales isn’t confined to a single product segment but rather reflects a wider market trend affecting the traditional bunker fuel landscape.

The picture for alternative fuels presented a mixed bag. Biofuel sales registered a third consecutive monthly drop, a surprising development given the industry’s increasing focus on decarbonization. This occurred despite a record volume of B100 being sold in May, indicating potential shifts in blend ratios. Conversely, Liquefied Natural Gas (LNG) bunker sales showed strong growth, rising to their highest level since January 2023. This surge in LNG uptake suggests a growing preference for this alternative fuel, aligning with environmental goals. However, no methanol sales have been recorded since February 2026, highlighting the nascent and somewhat unpredictable nature of emerging marine fuel markets within the Singapore bunkering hub.

Singapore’s Bunkering Market: A Year-to-Date Perspective and Future Outlook

Despite the weaker year-on-year performance in May, Singapore’s marine fuel sales over the first five months of 2026 paint a more optimistic picture. Total sales reached 23.3 million metric tonnes, representing a healthy 5% increase from the 22.2 million metric tonnes recorded in the corresponding period last year. This strong year-to-date performance suggests that while monthly fluctuations are normal, the overall trajectory for Singapore’s bunkering hub remains robust, demonstrating its resilience and continued dominance in the global shipping fuel market. The year 2025 was a landmark, achieving a record annual total of 56.2 million metric tonnes in marine fuel sales. If the first five months’ sales levels were to persist, the city-state would be on track to match or even slightly exceed this record.

This sustained year-to-date growth, even amidst monthly dips, underscores the fundamental strengths of the Singapore bunkering ecosystem. Its strategic location, efficient port operations, and comprehensive range of fuel offerings continue to attract a vast number of vessels. The commitment of the Maritime and Port Authority of Singapore (MPA) to innovation, digital transformation, and the development of greener fuels further cements its long-term competitive advantage. The ability of the Singapore shipping fuel market to adapt to new regulatory landscapes and embrace alternative energy sources is crucial for maintaining its leadership position in the global maritime industry.

Global Context and Regional Dynamics Influencing Bunker Demand

The dynamics observed in Singapore’s bunker sales are rarely isolated; they often reflect broader trends in global maritime commerce and regional economic conditions. The initial surge in bunker demand in March, triggered by the Iran war, serves as a stark reminder of how geopolitical tensions can swiftly alter shipping patterns and fuel procurement strategies. Such conflicts can lead to rerouting of vessels, increased sailing distances, or a heightened sense of urgency to refuel in stable, reliable hubs like Singapore, thereby temporarily boosting local demand for marine fuel. Conversely, a stabilization of these situations or changes in global trade flows can just as quickly temper demand.

Beyond geopolitical factors, global economic indicators play a significant role. A slowdown in international trade, reduced manufacturing output, or lower consumer demand can directly translate into fewer vessel movements and, consequently, lower overall bunker demand. The intricate global supply chain means that a ripple effect from one major economy can impact shipping activity across the world, including the demand for marine fuel in key bunkering locations such as the Singapore bunkering hub. Additionally, competition from other regional ports and evolving operational strategies of shipping companies, such as slow steaming, consistently influence sales volumes. Singapore must continuously monitor these multifaceted global and regional dynamics to maintain its competitive edge in the shipping fuel market.

Navigating Future Trends and Maintaining Singapore’s Bunkering Leadership

Looking forward, the Singapore bunker sales landscape will likely remain a focal point for the global maritime industry. While the May figures present a temporary dip, the robust year-to-date performance and the strategic initiatives undertaken by the MPA suggest a resilient and forward-thinking hub. The increasing adoption of LNG as a marine fuel, despite fluctuations in biofuel sales, points towards a growing momentum for decarbonization solutions. Singapore’s proactive efforts in developing infrastructure for alternative fuels, including its exploration of ammonia and methanol bunkering, will be pivotal in shaping the future of sustainable shipping. These developments are not just about meeting regulatory requirements but about fostering a greener and more efficient global shipping fuel market.

The challenge for Singapore lies in balancing traditional marine fuel sales with the accelerating transition to lower-carbon alternatives. This requires continued investment in infrastructure, technological innovation, and workforce development to ensure that the Singapore bunkering hub remains at the forefront of the industry. Engaging with shipping lines, fuel suppliers, and technology providers will be key to understanding evolving needs and driving collaborative solutions. As the global shipping industry navigates complex economic headwinds, geopolitical uncertainties, and ambitious decarbonization targets, Singapore’s ability to adapt and innovate in its marine fuel sales and supply operations will be critical to its enduring leadership in maritime commerce. The detailed analysis of monthly and year-to-date trends provides valuable data for all stakeholders involved in the dynamic and essential shipping fuel market.