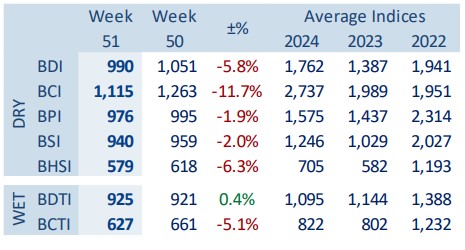

Tanker Market: The State of Affairs

As we enter 2025, it’s worth reflecting on the course of the tanker market during 2024, as well as giving an insight into what to expect in 2025. In a recent weekly report, shipbroker Xclusiv said that “the tanker market in 2024 exhibited remarkable resilience, achieving sustained profitability amidst considerable market volatility across various vessel segments. The following retrospective analysis delves into the year’s market dynamics, drawing insights from the Baltic Exchange’s TCE data. In the crude tanker sector, we witnessed larger vessels experiencing peak earnings early in the year”.

According to Xclusiv, “VLCCs which started 2024 strongly, reached their zenith on Feb 16th with a TCE rate of $65,537/day. However, the segment has since experienced a gradual decline, currently (18th Dec) being at $24,357/day – marking both a 19% decrease from the year’s start and the segment’s lowest point in 2024. Suezmax tankers followed a similar pattern, reaching their peak even earlier than VLCCs with TCE rates hitting $67,219/day on 17th Jan. The segment faced its challenging period in September, touching a low of $22,224/day on Sept 6th. However, showing remarkable resilience, rates have since rebounded and currently stand at $28,289/day – while this represents a 44% decrease from the start of the year, it’s notably 27% above the year’s lowest point. The Aframax segment has demonstrated particularly interesting dynamics. After reaching an impressive peak of $79,979/day on 16th Jan, rates experienced a significant correction, bottoming out at $19,954/day on 25th Sept. However, the segment has shown strong recovery, with current rates at $36,160/day – though this is 22% lower than the year’s start, it represents an impressive 81% increase from the year’s lowest point”.

Source: Xclusiv

Meanwhile, “the clean tanker market has told a tale of two regions. The Atlantic MR segment has been a stellar performer, currently trading at $37,300/day, marking a 34% increase from the start of the year. The segment reached its peak of $53,372/day on 31st May and, despite touching a low of $15,694/day on 30th Sept, has rebounded impressively to levels 138% above the year’s lowest point. In contrast, the Pacific MR market has faced more challenges. Current rates of $16,415/day represent a 42% decrease from the year’s beginning. While the segment saw impressive heights of $59,894/day on 31st Jan, it later experienced a significant downturn, reaching its lowest point of $11,218/day on 5th Nov. Current rates, while 46% above the year’s lowest point, reflect the continued challenges in this region. This varied performance across segments and regions underscores the complex dynamics at play in the tanker market throughout 2024, with each segment responding differently to market forces while maintaining overall profitable levels”, Xclusiv said.

“MR2 vessels have been the primary driver of tanker S&P activity, responsible for nearly more than one-third of all sales. The Aframax/LR2 segment comes in second, with 61 sales, 33 of which were product tankers. The increasing preference for clean trading options has significantly boosted the demand for MR2/LR2 vessels. Their versatility in handling both clean and dirty cargoes make them attractive to a diverse range of shippers and traders. From Jan to Nov 2024, we saw 562 newbuilding orders placed. However, only 7% of these orders were signed in Q4 so far. Q2 2024 witnessed the highest number of newbuilding orders for the year, with 259 orders. However, since Q3, we have observed a decline in the number of orders. One reason that may explain the decline in newbuilding activity is the availability of shipyard slots and the delivery schedules of vessels currently under construction. Approximately 13% of the 562 tankers ordered in 2024 are scheduled to be delivered in 2028 or later”, the shipbroker concluded.

Nikos Roussanoglou, Hellenic Shipping News Worldwide