LNG Shipping Trade: China’s Imports Keep Increasing

China’s LNG imports kept rising during 2024, following the trend of the previous years, but EU remains ahead. In its latest weekly report, shipbroker Banchero Costa said that “global seaborne LNG trade was increasing sharply until 2022, helped also by the events in Ukraine which forced Europe to diversify away from Russian pipeline gas. The last two years, however, have seen a significant slowdown in the growth levels. In Jan-Dec 2023, global shipments of LNG increased by just +1.4% y-o-y to 408.7 mln t, based on Refinitiv/LSEG vessel tracking data. In Jan-Dec 2024 there was no growth at all, with shipment volumes flat +0.0% y-o-y at 408.8 mln t. The largest exporter of LNG is now the USA, which accounted for 21.5% of shipments in 2024, followed by Australia with 20.0%, Qatar with 18.9%, South-East Asia with 11%. In Jan-Dec 2024, the USA exported 88.1 mln tonnes of LNG, which represented a -0.8% y-o-y decline from the 88.7 mln t shipped in 2023. Australia shipped 81.7 mln tonnes in Jan-Dec 2024, up +1.1% y-o-y. Qatar exported 77.2 mln tonnes in Jan-Jun 2024, down -2.1% y-o-y. From South East Asia shipments increased +7.2% y-o-y to 46.3 mln t. Russia shipped 31.9 mln tonnes of LNG in 2024, up +3.4% y-o-y from 30.9 mln t in 2023, but below the 32.9 mln t exported in 2022.

Source: Banchero Costa

According to Banchero Costa, the European Union remains the world’s largest importer of LNG. In 2024, the EU imported 83.2 mln tonnes of LNG, down -18.3% y-o-y, accounting for 20.4% of global LNG imports. The United Kingdom imported 7.6 mln tonnes of LNG in 2024, down -48.8% y-o-y from the 14.9 mln t in 2023, and almost two-thirds down from the 19.4 mln imported in 2022. Mainland China imported 78.7 mln tonnes of LNG in 2024, +10.2% y-o-y from 71.4 mln t in 2023. Japan imported 67.4 mln t in 2024, up +0.9% y-o-y. South Korea imported 47.8 mln t in 2024, up +5.3% y-o-y. India imported 25.5 mln t in 2024, up +21.0% y-o-y”.

“In 2021, Mainland China emerged briefly as the largest importer of LNG in the world, with a 20.7% share. In 2021, China’s imports jumped by +17.8% y-o-y to 79.0 mln tonnes. It overtook Japan, which in 2021 recorded a more modest +2.8% y-o-y increase to 76.5 mln tonnes. In 2022, however, there was a dramatic turnaround, as high gas prices and weak manufacturing due to COVID-19 lockdowns reduced demand for the fuel, whilst Western Europe rushed to replace pipeline gas supply from Russia. In 2022, China’s LNG imports declined by -18.7% y-o-y to 64.3 mln t. As such, it was again overtaken by a more stable Japan, which recorded a modest -3.8% y-o-y decline to 73.6 mln t, from 76.5 mln t in 2021. In 2022, both China and Japan got leapfrogged by the European Union, whose LNG imports surged by +67.6% y-o-y in 2022 to 100.1 mln tonnes, from 59.7 mln t in 2021. In 2023, Chinese imports rebounded strongly by +11.1% y-o-y to 71.4 mln t as Zero-Covid got shelved”, the shipbroker said.

Source: Banchero Costa

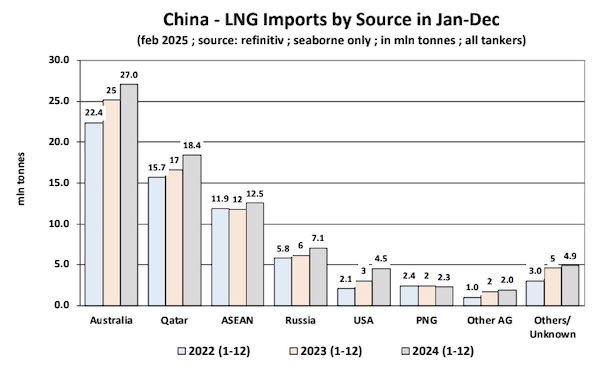

“In 2024, Chinese imports again increased by +10.2% y-o-y to 78.7 mln t, but it was not yet enough to overtake EU imports. In terms of sources for LNG shipments into China, the dominant player is always Australia. In Jan-Dec 2024, China imported 27.0 mln tonnes of LNG from Australia, up +7.6% y-o-y from the 25.1 mln tonnes in 2023, although this is still below the 31.0 mln t imported from Australia in 2021. Australia remains the top supplier to China, with a 34.4% in 2024. Shipments from Qatar to China increased +11.0% y-o-y in 2024 to 18.4 mln t, building on the +76.4% yo-y surge recorded in 2022 and the +5.9% y-o-y increase in 2023. Qatar now accounts for 23.4% of China’s total LNG imports in 2024. Imports to China from ASEAN (Malaysia and Indonesia) increased by +6.5% y-o-y in 2024 to 12.5 mln t. Volumes from Russia to China increased last year by +15.0% y-o-y to 7.1 mln t from 6.1 mln t in 2023. Finally, shipments from the USA to China rebounded by +48.3% y-o-y to 4.5 mln t in 2024”, Banchero Costa concluded.

Nikos Roussanoglou, Hellenic Shipping News Worldwide