Chinese Built Ships Calling on US Ports: Uncertainty is Still Prevalent as Deadline Nears

Uncertainty is still prevalent among the shipping industry, when it comes to the enforcement of the USTR directive aimed at restricting Chinese-built ships from calling on US ports. In its latest weekly report, shipbroker Gibson said that “in April, the Office of the United States Trade Representative (USTR) published their much-anticipated action plan to address alleged Chinese maritime dominance. Few further details have come to light since, and significant uncertainty remains around details of the policy. The measures are scheduled to come into effect soon, on the 14th of October, after a phase in period of 180 days. Briefly speaking, fees are planned to be imposed for making port calls in the US based on whether a vessel is Chinese built or Chinese owned or operated. For a Chinese owned or operated vessel, an initial tariff of $50 per net tonne (NT) per port call or rotation of US port calls applies, with no exemptions, increasing over the next three years. These vessels would in effect be excluded from the US market, as the costs incurred would make these vessels uncompetitive”.

According to Gibson, “for Chinese built, but not owned or operated vessels, the measures are more complex as various exemptions may apply. Regardless of vessel size, if the tanker arrives in ballast, the voyage is less than 2000nm, the vessel is less than 55,000 dwt, or it is US beneficially owned, no fees will apply. Note that the 80,000 dwt bulk capacity threshold exemption hasn’t been clarified, though it is mostly interpreted as applying only to dry bulk vessels below 80,000 dwt. Provided none of these exemptions apply, US port calls on a Chinese built vessel would be impacted, and a fee of $18/NT is set which is also set to increase over the next three years. Significant uncertainty remains around details, including any potential costs incurred or avoided by re-berthing or discharging via STS”.

Source: Gibson Shipbrokers

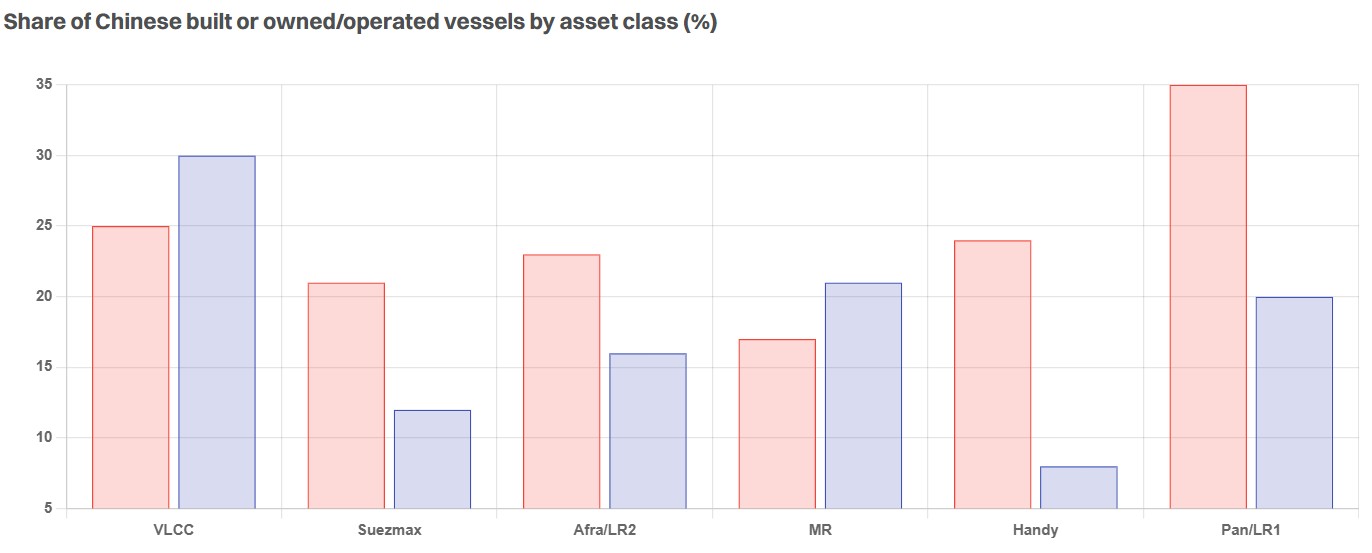

“As it stands, vessels subject to Chinese lease financing are expected to be classified as Chinese owned, and here a significant impact has already been felt. Substantial efforts to diversify away from facilities with Chinese lessors have been seen in recent months, as lessors are facing early repayments and lower demand. Law firms are exploring structures to retain Chinese lease facilities and circumvent the Section 301 regulations, though a readily applicable solution has yet to be found. The total numbers of vessels affected depends on what definition is used for Chinese owned or operated. If the definition is applied liberally, around 19% of the tanker fleet greater than 25,000 dwt are Chinese owned or operated, though most of these operate East of Suez and are unlikely to trade to the US. We are currently counting over 500 tankers on the water above 55,000 dwt which are Chinese built but not Chinese owned or operated, of which again most are trading East of Suez. Note that these are indicative numbers, as the USTR’s definition of owner or operator of a vessel is yet to be fully clarified. Further, nearly 70% of the current tanker orderbook greater than 25,000 dwt is on order in China”, the shipbroker said.

Gibson added that “nearly 90% of clean trade into the US is carried on vessels below 55,000 dwt and is thus exempt. US imports of clean products on vessels over 55,000 dwt have totalled less than 100kbd so far this year, most of which from ports further than 2000nm distance, a volume that can be replaced. On the dirty side, the US imports significant volumes of Crude/DPP on vessels over 55,000 dwt from areas more than 2000nm from US ports, including from the parts of Latin America such as Brazil and Argentina. These will all face fees if carried on Chinese built vessels”.

“There is significant uncertainty around who will foot the bill, with reports of both charterers and shipowners adding provisions to cover potential costs. In cases where vessel availability is tight, yet a Chinese built vessel is available, instances have been recorded where charterers have been forced to compensate owners. In turn, weaker markets may see owners take the hit, if other trading possibilities prove less lucrative. Consequently, fixtures enabling Chinese linked ships to leave the US and resume trading elsewhere have been noted. We are further observing discounts for TCs on Chinese owned/operated ships. So far, the full impact of USTR Section 301 is difficult to ascertain due to a lack of clarity on the many open questions remaining. However, if implemented in its current form, it seems clear that Chinese built tankers above 55,000 dwt will be less likely to trade to the US. Further, Chinese owned and operated vessels will be forced to steer clear of US trade. While the share of Chinese built, owned or operated ships is significant, it would appear there are enough ships without a Chinese connection to service US demand. However, volatility in freight rates cannot be ruled out as supply chains adjust to the new rules”, the shipbroker concluded.

Nikos Roussanoglou, Hellenic Shipping News Worldwide